Whitepaper

At the cross-border crossroads

At the cross-border crossroads

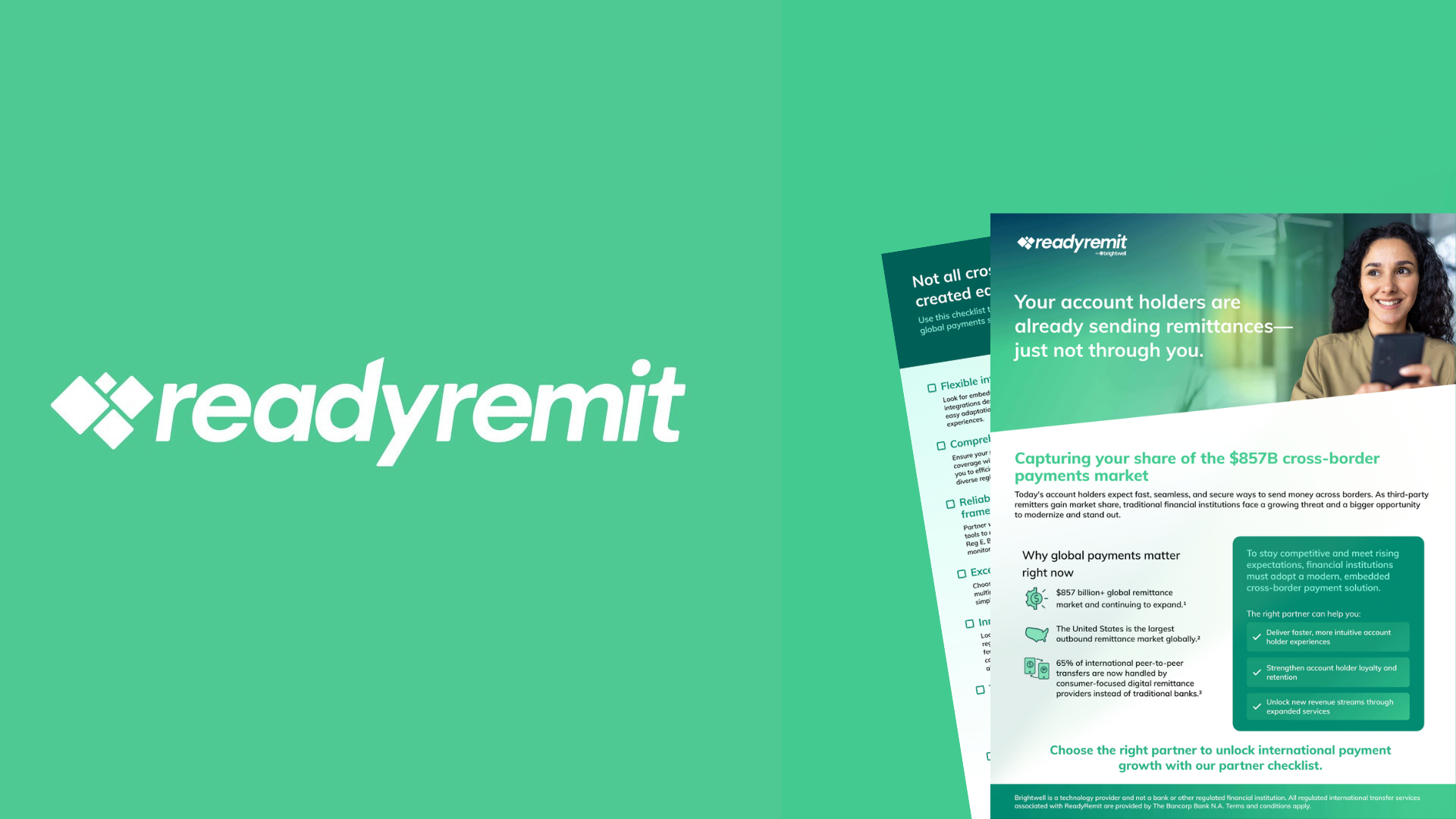

As cross-border payments shift from a niche offering to a core driver of loyalty, financial institutions that fail to modernize risk becoming invisible in their customers’ financial lives. Those that act now can capture growth, deepen trust, and secure long-term account primacy in an increasingly competitive landscape.

In this white paper we will explore how:

- Fintechs and neobanks now dominate cross-border flows, quietly eroding traditional financial institution revenue and relevance.

- "Silent attrition” is accelerating as account holders migrate to providers offering modern, real-time experiences.

- Modernizing cross-border capabilities strengthens loyalty, increases deposits, and differentiates financial institutions in a crowded market.

- Low-lift, white-label solutions allow banks and credit unions to offer fast global payments without major IT burdens or compliance risk.

.png)

As cross-border payments shift from a niche offering to a core driver of loyalty, financial institutions that fail to modernize risk becoming invisible in their customers’ financial lives. Those that act now can capture growth, deepen trust, and secure long-term account primacy in an increasingly competitive landscape.

In this white paper we will explore how:

- Fintechs and neobanks now dominate cross-border flows, quietly eroding traditional financial institution revenue and relevance.

- "Silent attrition” is accelerating as account holders migrate to providers offering modern, real-time experiences.

- Modernizing cross-border capabilities strengthens loyalty, increases deposits, and differentiates financial institutions in a crowded market.

- Low-lift, white-label solutions allow banks and credit unions to offer fast global payments without major IT burdens or compliance risk.